Ever since I wrote a post on LinkedIn a few days back on how much one should be increasing one’s annual income, I have been flooded with questions, clarifications, and scenarios that can help elaborate my post.

I was not surprised to see that the majority of the questions were on how to invest, assets to focus on while investing, and sources of additional income. But, few people reached out to me to get my input on assets in which I have invested the least and the rationale behind them. So here is my take:

*** Before reading further, please be aware that these are my opinions and inputs based on what I have learned. By no means am I claiming that I am a financial expert 🙂 ***

Investing in automobiles:

A car depreciates by around 20-30% the moment you drive it out of the showroom. Imagine buying a 10 Lakh car in the showroom and driving out with a value of 7.5 Lakhs. That’s how fast it depreciates. Add the road tax, insurance, and other taxes, and it undoubtedly is one of the assets that I am not a big fan of. The worst situation would be when you take a car loan to finance it – you will end up spending another 8-10% as interest. But this does not mean that you should not own a car. End of the day, we need a vehicle – the balance that you need to strike is to buy the right car that suits your need and stick with it for a good time. Changing cars just for sake of experience and status might not be a smart idea for the above reasons.

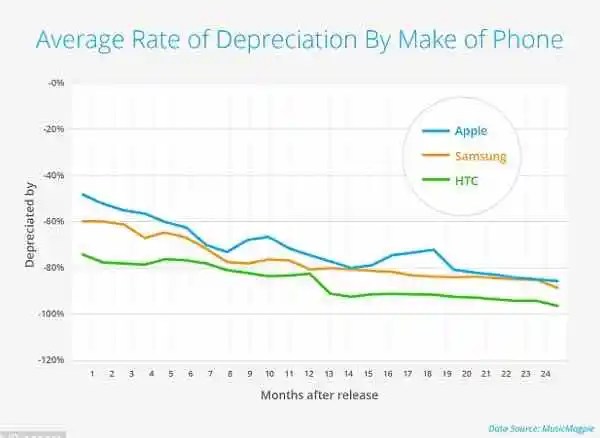

Electronics and high-end Gadgets:

I am a big fan of technology, but I am also aware that with the rate at which technology is evolving, the gadgets that we hand in our hands today become obsolete very quickly. Don’t be surprised if I tell you that the 1 Lakh + phones that you carry would have depreciated by a whopping 80-90% in just 2 years. I usually stay away from changing my mobile for the sake of it and yes I usually stay away from high-end phones.

I have stayed away from personal loans:

I have always been skeptical when it comes to personal loans for 2 reasons – one, the rate of interest is usually very high and two, it gives a false sense of having high cash flow. Before you know what hit you, you are in this vicious circle of managing high payout debt. I would rather put off my vacation plan to an exotic island than take a personal loan to book one

Frequent upgrades of your home:

Don’t get me wrong, I am not commenting on the appreciation that we associate with real estate, I am referring to the costs that we incur when we upgrade our homes. Imagine the money that we have to shell out on the registration costs and interior designs – In today’s world, they can easily add up to almost 20% of the price of the house. If you keep upgrading your house frequently to reflect your current lifestyle or status, this will start hurting you.

Be smart with those credit cards:

I firmly believe in paying out in full all my credit card bills. For all practical purposes, I look at my credit cards as “Debit cards”. I only swipe the card if I am confident that I can pay it off during that billing cycle.

Lifestyle

And finally, I have to focus on the lifestyle. As your income increases over the years, it is natural that you are going to be spending more on – travel, experiences, and hobbies. But one key parameter to keep a tab on is the (Annual expenses / Annual Income) ratio. As you start your career, this factor might be close to 1 as you might not be saving much or you are barely meeting your needs. But as you start growing in your career, this number should start decreasing. Do not keep this factor at 1 i.e. your expenses grew at the same rate as your annual income.

I am not asking everyone to live a life of a monk :). I don’t do it myself – I spend a lot on travel, and I spend a decent amount of money on entertainment and experiences, but I refrain from a few of the points that I have called out above